Understanding the relationship between deductible vs premium reduces the chances of making a wrong choice during policy purchase. While deductible and premium are both insurance charges, they are dissimilar and serve different purposes. However, they still have an inverse relationship every new policyholder must know about.

After getting familiar with these terms and how they work, then striking a balance that’s unique to your needs is next. This article helps you compare these charges as individual components while shedding light on their connection to prepare you for decision-making

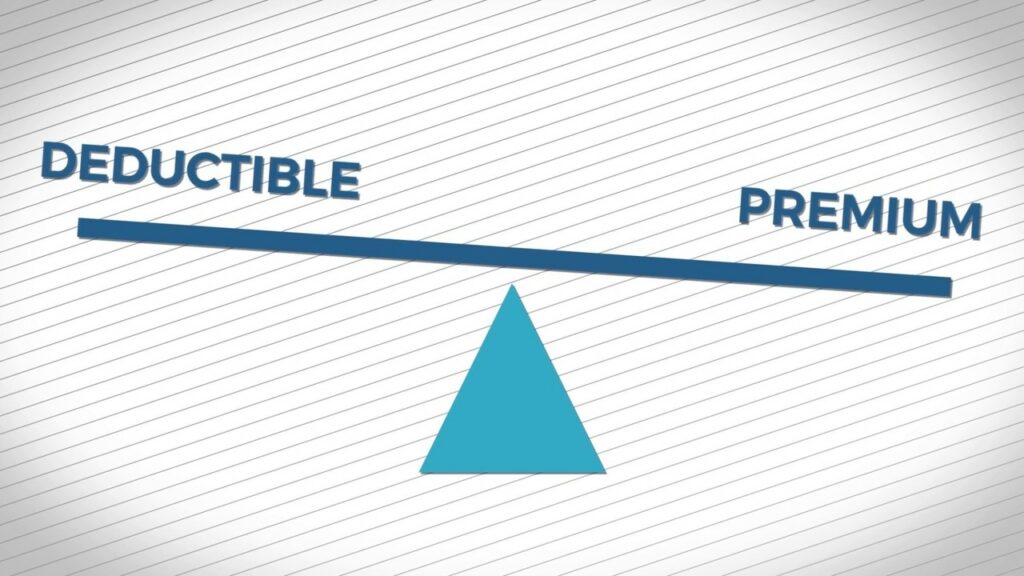

Overview of deductible vs premium

An insurance premium is the price for signing an insurance contract. Your risk profile and choice of policy determine the premium price you pay. Making unnecessary payments for premiums outside your special needs may lead to over-insurance.

While a deductible is an out-of-pocket expense, you pay for a claim before getting your insurance benefits. It doesn’t change but maintains a set amount for each claim you file on your plan. This payment is a risk-sharing method between you and your policy provider.

As I earlier said, there is a relationship between both charges. The amount of the deductible affects the premium. When the deductible is high, the premium is reduced, and vice versa. This is a necessary balance that ensures plans don’t become too expensive to maintain.

However, it’s up to you to decide how to create this balance; your situation determines which charge you prioritize. In health insurance, individuals with conditions that require frequent medical attention need a lower deductible.

What are the pros and cons of deductible vs premium?

Another way to identify additional details in our study of deductible vs premium is to learn about their pros and cons, which refer to the benefits and downsides of these charges.

Deductibles

Advantages of deductibles

- Lower premiums: The good thing about the deductible is you can use it to adjust the amount for premium. All you need to do to lower your premium is spend more on deductible

- Financial security: If you meet your deductible, your insurers will cover the remaining expenses. This means that you can contribute to your financial stability as a policyholder.

- Ability to manage expenses: You can also devise a plan to meet your limits. Either you spend on expensive services or manage your cut round the year. The choice is yours.

Disadvantages of deductible

- Higher out-of-pocket costs: Premium for medical insurance costs less than other policies. This means that you will cover most of your expenses from your pocket.

Premium

Advantages of premium

- Provides access to coverage: Premiums are the most important charges on your insurance plan. They’re the payment you make in exchange for a policy, an investment in coverage, and financial protection.

- Encourages risk sharing: When you pay premiums to access coverage, you sign up for a risk-sharing relationship with your policy provider. This means you no longer have to experience financial strain from expenses.

Disadvantages of premiums

- Waiting periods: Not all insurance benefits kick in immediately after you pay your premium. Some insurers require you to wait three to thirty-six months to enjoy full coverage.

- Uncertainties: One thing premium doesn’t do is prepare you for unforeseen circumstances. This may include premium increases which happen in time for renewal or claim denials from insurers

- Costly: We already know that the premium is the insurance price. Sometimes, this price becomes too expensive to maintain. If you have no proper plan, it can affect your budget.

Conclusion

To conclude, this article is an illuminating study of deductible vs premium. Piece by piece, it answers questions concerning these insurance components to eliminate difficulties in your insurance plan.

Share the article with others if you find it helpful.

Conversation

0 Comments